Quick Summary: Thinking of building a fintech app in 2026, you’re entering a market that’s grown far past the early wave of mobile wallets and basic payment tools. Adoption is near universal, AI is now baked into the main fintech infrastructure, and regulators are paying closer attention than ever. This blog walks through the actual development process, what it costs at different complexity levels, the compliance standards you can’t skip, and how to pick a development partner who won’t leave you exposed on timelines or security.

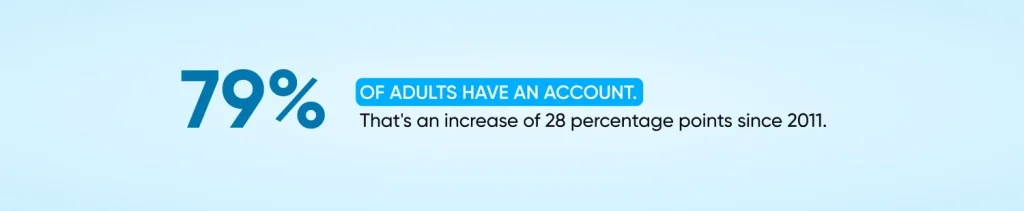

Financial access has reached a point most founders building five years ago couldn’t have planned around. As per the World Bank’s Global Findex Database, 79% of adults globally now have a financial account, which means the audience for a new fintech product isn’t a niche group anymore; it’s most of the addressable internet. That’s the opportunity side.

The harder part is that everything is the underlying infrastructure of a good fintech app: choosing a tech stack that can actually scale, meeting compliance standards that change by region and product type, and pricing the build accurately before you commit a budget. If you’re trying to build a fintech app right now, the real questions aren’t “is this a good idea?” They’re about cost, timeline, security, and who you build it with. That’s what this guide covers.

What Is a Fintech Application?

A fintech application is software that delivers financial services or tools through a mobile or web interface, things like payments, lending, investing, banking, or insurance, often replacing or extending what a traditional bank branch used to handle. Modern fintech apps are usually built on cloud infrastructure, lean heavily on third-party APIs for banking and payment rails, and increasingly use AI for fraud detection, credit decisions, and personalization. The category covers everything from building a peer-to-peer payment app tool to a full neobanking platform, and the technical and regulatory bar has risen sharply for all of them.

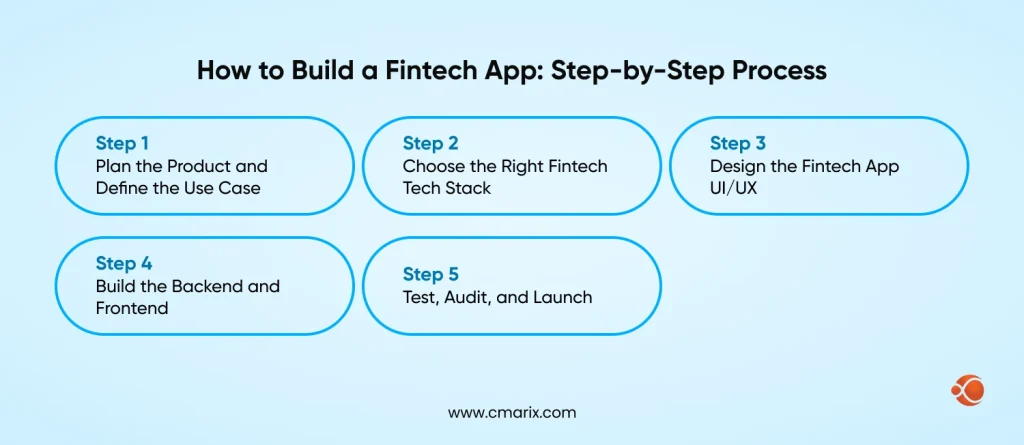

How to Build a Fintech App: Step-by-Step Process

Here’s how the fintech app development process actually breaks down once you move past the idea stage. Each step has its own decision points, and skipping ahead on any of them is usually what causes delays later.

1. Plan the Product and Define the Use Case

Before any code gets written, you need clarity on the exact problem you’re solving, who you’re solving it for, and what regulatory category your product falls into. This single decision shapes almost everything downstream.

- What specific financial problem does the app solve, and for whom?

- Which regulatory category does it fall under (payments, lending, wealth management, insurance, banking-as-a-service)?

- What licenses or registrations does that category require in your target markets?

- What does the competitive landscape already offer, and where’s the actual gap?

Getting this stage wrong is expensive. A lending product, for example, carries entirely different compliance obligations than a budgeting app, and that difference affects your timeline, your cost, and which technology partners you’ll need.

2. Choose the Right Fintech Tech Stack

Your fintech tech stack must handle security, scalability, and speed simultaneously, setting a much higher standard than most consumer apps.

The table below outlines how stack decisions typically break down by layer.

| Layer | Common 2026 Choices | Why It Matters |

| Cloud infrastructure | AWS, Google Cloud, Azure | Compliance certifications, scalability, and built-in security tooling |

| Backend language | Python, Java, Kotlin, Node.js | Reliability under transaction load, mature security libraries |

| Mobile framework | Native (Swift/Kotlin) or Flutter | Speed to market vs. platform-specific performance |

| API layer | REST/GraphQL with API gateway | Clean integration with banking, KYC, and payment partners |

| Data layer | PostgreSQL, encrypted cloud storage | Auditability and compliance with data protection standards |

API-first architecture matters more than the specific language choice, since it lets you plug in banking and payment partners without rebuilding core logic every time a regulation or provider changes. Teams moving fast on payment products are also increasingly choosing frameworks built for quicker iteration across platforms.

For a real example of this in practice, see how fintech startups in Africa are choosing Flutter for faster payment app development to ship cross-platform products without doubling their engineering effort.

3. Design the Fintech App UI/UX

Fintech app design has its own rules, because users are trusting the interface with their money, not just their attention. A few principles tend to separate trustworthy fintech design from generic app design:

- Clarity over decoration. Every screen should make the next action obvious, especially around payments, transfers, and confirmations.

- Immediate feedback. Users need to know instantly whether a transaction succeeded, failed, or is pending. Silence reads as a bug.

- Consistency. Typography, color, and iconography need to stay uniform across the entire app, since inconsistency reads as untrustworthy in a financial context specifically.

- Accessibility. Financial apps serve a wider age and ability range than most consumer products, so contrast, font sizing, and screen-reader support aren’t optional polish.

Wireframing and prototyping before development starts is worth the extra week, since usability issues are far cheaper to fix on paper than after the backend is built around a flawed flow.

4. Build the Backend and Frontend

This is the stage where card issuing and payment processing get wired in, along with core banking logic, authentication, and data storage. Three things tend to define this phase:

- API integration is the backbone of most fintech builds, since teams rarely build payment rails, KYC checks, or credit bureau connections from scratch. Integration quality here determines both your launch timeline and your long-term maintenance burden.

- Digital payment app development at this stage means supporting multiple payment methods, cards, bank transfers, and wallets, rather than betting on just one rail.

- Authentication and authorization need to be built with financial-grade security from day one, not retrofitted after a security review flags gaps.

5. Test, Audit, and Launch

Security testing here goes beyond standard QA. It needs to include a compliance review, penetration testing, and load testing under realistic transaction volume before you go live. A vulnerability found after launch is far more expensive and far more damaging to user trust than one caught in this stage.

Trust CMARIX to handle the tech and the legal aspects.

Building Your Fintech Startup MVP: What to Include First

If you’re still validating the idea, you don’t need every feature from the process above on day one. A fintech startup MVP should cover one core transaction flow done well, basic but secure authentication, and just enough compliance groundwork to operate legally in your target market.

A well-scoped MVP usually includes:

- Secure user onboarding with basic KYC

- One primary transaction flow: a single payment type, one lending product, and one investment instrument

- A minimal but functional dashboard or account view

- Enough audit logging to satisfy early compliance checks

The goal is to get real user behavior data with the smallest build that still feels trustworthy to someone handing over financial information. Many founders use this stage to test demand before tackling a full build, such as a P2P payment app, which keeps early costs low while still proving out the underlying model with real users.

Key Fintech App Features to Prioritize in 2026

Not each feature deserves equal investment at launch. Here’s where to focus, broken down by product category.

Banking and Neobank Features

If you’re building anything adjacent to digital banking, the following have become baseline expectations rather than differentiators:

- Account aggregation across various linked banks

- Virtual and physical card issuing

- Automated budgeting and savings tools

- Real-time spending insights and categorization

- Instant notifications on every transaction

For a deeper look at what this category demands specifically, see our guide on Neobank app development.

Lending and Cash Advance Features

Short-term lending and cash advance products have become one of the fastest-growing fintech categories, largely because they solve an immediate, well-defined user need. Core features in this space typically include instant eligibility checks, transparent fee disclosure, flexible repayment scheduling, and automated underwriting using alternative credit data. If this is your space, it’s worth studying how existing players structure their flows. Our breakdown of cash advance apps like MoneyLion covers the feature set users expect from a credible competitor in this category.

Wealth and Investment Features

Robo-advisory tools, portfolio tracking, automated rebalancing, and goal-based investing have moved from “nice to have” to standard in investment products. Users increasingly expect a level of personalization that used to require a human advisor. If you’re scoping this category, our guide on how to create an investment platform walks through the feature priorities in more detail.

Blockchain and AI in Fintech

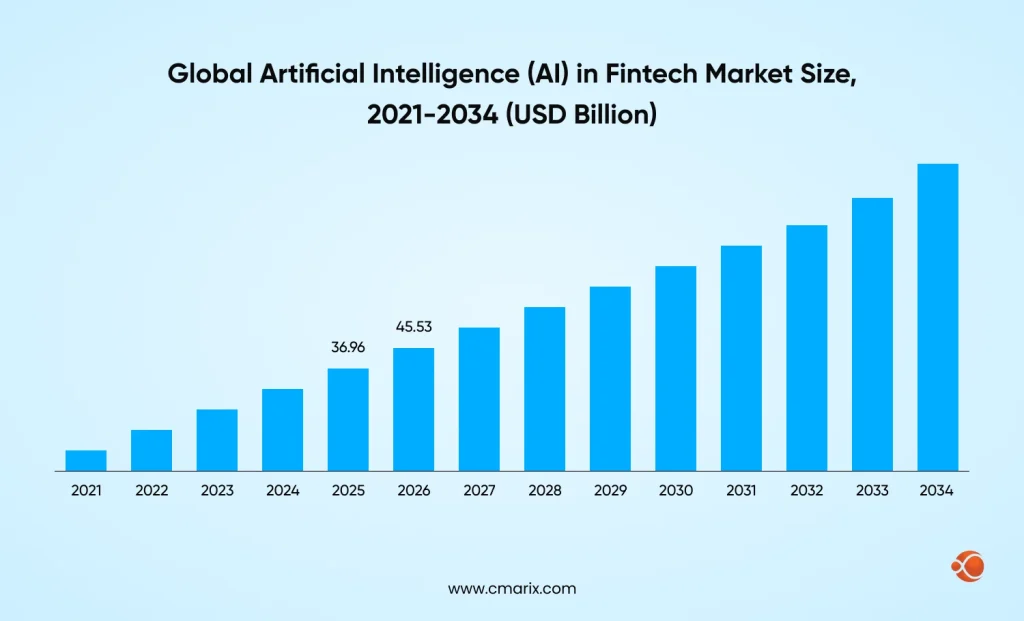

AI is no longer an add-on in fintech; it’s infrastructure. The global AI in fintech market was valued at USD 36.96 billion in 2025, according to Fortune Business Insights, and that growth is being driven directly by fraud detection, credit scoring, and personalization use cases. Practical applications worth budgeting for include real-time transaction fraud scoring, AI-assisted credit decisioning, conversational support for account queries, and personalized financial recommendations based on spending patterns.

Blockchain still plays a role in specific niches, cross-border payments, and settlement transparency in particular, but its application in 2026 is far more targeted than the broad hype it carried a few years ago. Most fintech apps don’t need blockchain at the core; they need it only where it solves a specific settlement or transparency problem.

Fintech App Development Challenges & Compliance

This is the section most founders underestimate, and it’s usually where timelines and budgets slip the most.

Financial Data Security

Security in fintech is not optional; it’s existential. The average cost of a data breach in the financial sector is $4.4 M, and continuous monitoring a budget line item from day one, not something bolted on before launch. At minimum, this means encryption at rest and in transit, role-based access controls, continuous anomaly monitoring, and a clear incident response plan that’s actually been tested, not just written down.

Compliance Standards You Need to Meet

Depending on your market and product type, you’ll likely need to meet several overlapping standards. AWS alone supports 143 security standards and compliance certifications, including PCI-DSS, HIPAA/HITECH, FedRAMP, GDPR, FIPS 140-3, and NIST 800-171, which gives a sense of just how layered fintech compliance has become.

| Standard | Applies When | What It Covers |

| PCI-DSS | You handle card data directly | Cardholder data storage, transmission, and processing security |

| KYC/AML | Nearly any app moving money | Identity verification and anti-money laundering checks |

| GDPR | You serve users in the EU | Personal data collection, storage, and user consent |

| FedRAMP | You serve US government-adjacent clients | Cloud security authorization for federal data |

| NIST 800-171 | Handling controlled unclassified information | Security controls for sensitive but unclassified data |

Not doing it properly is not only going to incur penalties; it will cause a delay of several months while you try to get things right retroactively. The teams that manage to move fast in their development processes are those that are able to identify their compliance needs early on.

How to Plan Your Fintech App Budget in 2026: Cost Breakdown

Cost is usually the first real-world question once planning gets serious, and it varies more than most generic estimates suggest, mainly because compliance and integration scope vary widely across product categories.

| Complexity Tier | Example Product | Estimated Cost Range | What Drives the Cost |

| Basic | Single-feature payment or remittance app | $40,000 – $80,000 | Minimal integrations, lighter compliance scope, single market launch |

| Mid-complexity | Lending app or investment app with KYC/AML built in | $80,000 – $180,000 | Multiple third-party integrations, broader compliance scope, and identity verification |

| High-complexity | Full neobanking platform or multi-product fintech suite | $180,000 – $400,000+ | Card issuing, multiple regulatory licenses, ongoing compliance monitoring, custom backend architecture |

These ranges assume a single-region launch with a standard feature set per tier. Multi-market compliance, custom card programs, or heavy AI integration can push the high end well past $400,000.

A handful of factors move the number more than anything else:

- Integration cost: Every payment processor, banking data API, or KYC vendor that you integrate requires more time spent developing and testing.

- Compliance scope: Operating across many markets amplifies the compliance burden because few requirements align neatly.

- Platform choice: Native apps for both iOS and Android cost more than a well-built cross-platform app, though performance tradeoffs exist either way.

- Custom backend logic: The more you build versus outsource to existing API providers, the higher the engineering cost, but also the more control you retain over your roadmap.

Working with an experienced fintech app development partner usually costs more upfront than a generic dev shop, but it tends to save money downstream by avoiding compliance rework and security retrofits later, which are almost always more expensive than building it correctly the first time.

Get pricing based on your features, scope, timeline, and goals.

How to Choose the Right Fintech App Development Company

A few things matter more than a polished portfolio here, and most of them come down to whether the company has actually shipped financial products, not just consumer apps.

- Domain-specific experience. Ask for examples of fintech products they’ve built, not general mobile app work. The compliance and security requirements don’t transfer over from other industries.

- Regulatory track record. Ask directly how they’ve handled PCI-DSS or KYC/AML integrations on past projects, and ask for specifics, not a general assurance that they’re “compliant.”

- Security practices. Find out whether penetration testing and security audits are a standard part of their process or something added only on request.

- Post-launch support model. Fintech apps need ongoing monitoring and updates as regulations shift, so ask what support looks like after launch, not just during the build.

- Case studies over claims. A company that can show real fintech case studies, ideally with measurable outcomes, is a stronger bet than one offering only general capability statements.

A company that can’t speak specifically to regulatory experience is a risk you don’t want to carry into a financial product, since the cost of fixing compliance gaps after launch is almost always higher than the cost of choosing the right partner upfront.

Why CMARIX for Custom Fintech App Development

CMARIX has built custom fintech app development solutions across lending, payment, and investment platforms for clients across 40+ industries. With hands-on experience in integrating KYC/AML checks and compliance frameworks like PCI-DSS into live products.

The team that works across the full stack, from API integration and cloud architecture to AI-driven fraud detection, which means security and compliance get built in from the planning stage rather than added on after a security audit flags a gap. That approach has shaped how CMARIX scopes every fintech engagement, with compliance treated as a planning input rather than a final checklist item. For example, CMARIX developed the fintech platform Eddbee, an investment and algorithmic trading solution supporting 60+ global stock markets, advanced portfolio management, stock screening, multi-currency operations, and enterprise-grade security standards across its infrastructure and APIs

Conclusion

Building a fintech app in 2026 means more than wiring up a payment flow and shipping it. The opportunity is real, with adoption now reaching the majority of the global population, but the bar on compliance, security, and AI-driven features has moved up just as fast.

Getting the tech stack, cost planning and development partner right from the start is what separates a fintech product that scales from one that stalls is what separates a fintech product that scales from one that stalls under its first compliance audit. If you’re ready to move from planning to building, talk to our fintech development team about your specific use case.

FAQs on Build A Fintech App

How do you build a fintech app?

Begin by defining your specific use case and regulatory category, then choose a secure, scalable tech stack and integrate the third-party APIs you need for payments, banking data, or KYC. From there, design the interface, develop the backend and frontend, and run thorough security and compliance testing before launch.

How much does it cost to build a fintech app in 2026?

Cost widely changes based on complexity. A simple payment app costs far less than a multi-feature lending or investment platform, and a full neobanking suite with card issuing and multiple licenses sits at the top of the range. Compliance scope, integration count, and platform choice(native vs cross-platform) are the biggest cost drivers.

What are the mandatory security and compliance standards for fintech apps?

PCI-DSS applies if you handle card data, KYC/AML checks are required for nearly any app moving money, and GDPR applies if you serve EU users. Depending on your cloud provider and market, you may also need to meet standards like FedRAMP, HIPAA/HITECH, or NIST 800-171.

How long does the development process take from idea to launch?

A basic MVP can launch in just a few months, while a full-featured fintech app with multiple integrations and compliance requirements usually takes 6 months to a year. Compliance review and security testing are often the stages that extend timelines the most.

Which third-party APIs are essential for fintech app functionality?

KYC/identity verification services, payment processing APIs, banking data aggregation APIs, and fraud detection tools are the core integrations most fintech apps depend on, along with card issuing APIs for products that need virtual or physical cards.

What are the key features of a Minimum Viable Product (MVP) for fintech?

A fintech MVP should focus on one core transaction flow executed well, basic but secure authentication, and the minimum compliance groundwork needed to operate legally in your target market, rather than trying to launch every feature at once.

How do I monetize my fintech application?

Common models include interest or lending margins, transaction fees, subscription tiers for premium features, and partnership or referral revenue from integrated financial services. Most successful fintech apps combine 2 or 3 of these rather than depend on one.