Quick Summary: Custom algorithm trading software automates buy/sell decisions using predefined rules, removes human error, and allows split-second execution. This guide covers trading strategies, architecture decisions, a 5-step build process, and what risk management features you can’t skip.

Algo trading has moved well past the walls of large investment banks. Hedge funds, prop firms, and individual traders are all building or buying automated trading systems, and for good reason. A well-built trading algorithm software can process thousands of signals simultaneously, execute orders in milliseconds, and apply a consistent strategy without hesitation or fatigue.

But developing custom algorithm trading software is not a plug-and-play exercise. It requires precise and clear strategy definition, reliable data infrastructure, careful backtesting, and risk controls that are non-negotiable.

What Is Algorithm Trading Software?

A trading algorithm is a program that places buy or sell orders automatically when predefined market conditions are met. That could be a price crossing a moving average, a volume spike, or a spread between two correlated assets widening beyond a threshold.

The software monitors markets in real time, evaluates those conditions, and executes all orders without manual intervention. This removes emotional decision-making, reduces execution latency, and lets traders run strategies at a scale no human could manage alone.

The two main platform types:

- Commercial platforms: Off-the-shelf systems developed for retail traders. Think Binance, Robinhood, or MetaTrader. Easy to set up, limited in customization.

- Proprietary platforms: Custom-built systems designed around particular strategies and data requirements. Commonly used by prop desks, banks, and experienced independent traders. These platforms offer complete flexibility and are often created through custom trading software development to support specific workflows, analytics, and execution needs.

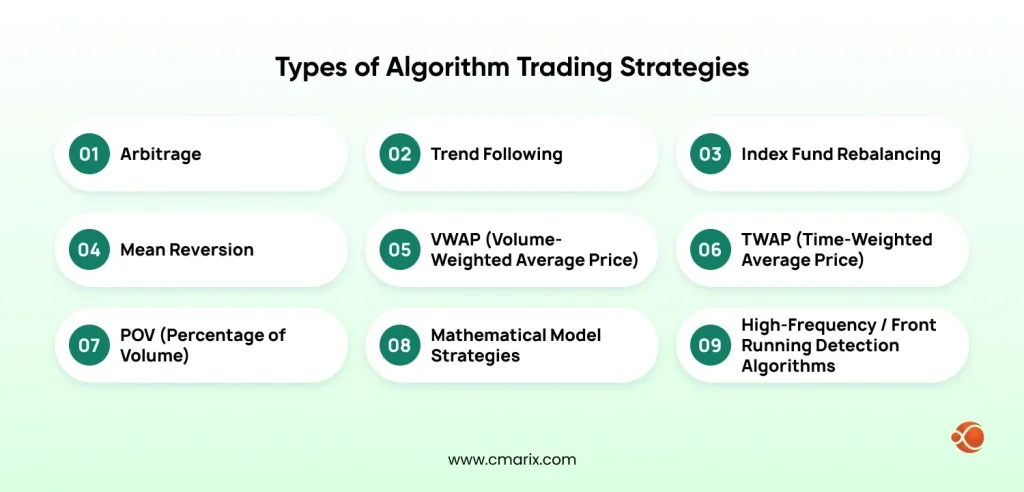

Types of Algorithm Trading Strategies

The strategy defines what the algorithm is actually watching for. Here are the most commonly implemented approaches:

- Arbitrage: It utilizes price differences for the same asset across two exchanges. The algorithm buys low on one and sells high on the other at the same time. Although margins are thin, the approach is basically risk-free if executed quickly.

- Trend Following: tracks moving averages, channel breakouts, and price levels. No price prediction required. The algorithm simply follows what the market is already doing. It is the most widely used strategy in algorithmic trading.

- Index Fund Rebalancing: index funds rebalance at scheduled intervals to maintain benchmark alignment. Algorithms can anticipate these rebalances and position accordingly.

- Mean Reversion: as per the idea that asset prices return to a historical average. If a stock drifts significantly above or below its average, the algorithm bets on a return to the mean.

- VWAP (Volume-Weighted Average Price): breaks large orders into smaller chunks timed around historical volume patterns to reduce market impact.

- TWAP (Time-Weighted Average Price): TWAP splits orders into equal time intervals rather than volume-based ones. Useful for reducing price impact on illiquid assets.

- POV (Percentage of Volume): links order size to live market volume. The algorithm participates at a fixed percentage of whatever volume is trading at that moment.

- Mathematical Model Strategies: delta-neutral and other quantitative models that balance positive and negative positions to reduce directional risk.

- High-Frequency / Front-Running Detection Algorithms: advanced systems that detect the presence of other algorithms in the market and respond accordingly. Used by sophisticated institutional players to avoid being gamed by other bots.

Choosing the right strategy is the first real decision. Every other technical choice, like data feed, execution speed, and backtesting approach, flows from it.

Our team has built algorithmic trading systems across various strategies.

How to Build Custom Algorithm Trading Software in 5 Steps

Step 1: Set Up Your Trading Platform

Before writing a line of strategy logic, you need an infrastructure layer that can pull in market data, store it, and run backtests against it.

Two paths here:

- Build around an existing API — broker APIs like Interactive Brokers or Alpaca give you market data and order execution. You write the strategy layer yourself.

- Use a backtesting framework — Python-based tools like Backtrader or Zipline are pre-built for testing strategies against historical data and connect to live exchanges. Faster to get started, but less flexible on execution.

If your goal is a production-grade system with custom data sources or proprietary execution logic, start with the API route and work with a team that knows trading software architecture.

Step 2: Define Your Strategy in Code-Ready Terms

This is where most projects get stuck. A strategy that sounds clear in a conversation often falls apart when you try to express it as concrete rules.

The test: can you draw it as a flowchart? If not, it cannot be coded. Every entry condition, exit condition, position size rule, and override scenario needs to be expressible as a logical if/then statement before development starts.

Make sure to outline your strategy clearly, including how you’ll place orders, when you’ll trade, and set price limits. Stick to the market rules as well. Just remember, currency pairs aren’t the same as stocks, so tactics vary by exchange.

Step 3: Choose Your Timeframe and Execution Frequency

Time frame is an important architectural input. It affects how much data you need, what latency is acceptable, and how frequently the system needs to compute.

High-frequency trading systems operate super fast, using microsecond data and requiring special co-location setups. Swing trading algorithms check conditions only once a day, though. Mid-frequency systems that fall in the middle use hourly or minute data but still manage sub-second latencies.

Your own availability matters too. An HFT system left unmonitored is a liability. Be realistic about how much oversight you can provide.

Step 4: Backtest Against Historical Data

Don’t ever trade real money using an untested algorithm. Backtesting lets you run your trading strategy against past market data, showing you how well it likely would have done. For good backtesting, you need to factor in slippage, commissions, and realistic fill rates – not just signal performance. If your algorithm seems profitable but doesn’t consider those costs, it could still end up losing money when you use it for real trades.

Watch out for overfitting: a strategy tuned too precisely to historical data will fail on new data. Use out-of-sample testing periods to validate that the strategy generalizes. Once backtesting results are satisfactory, move to a paper trading (demo) account that simulates real market conditions without real capital at risk.

Step 5: Go Live With Real-Time Monitoring

To connect your algorithm to a live trading account, use direct exchange links or your broken API for algorithmic trading. Remember, though, that while paper trading provides good results, these might differ from live trading due to the algorithm impacting the market and having different fill rates. So, keep a close watch during those first live runs.

Also, set up a stop mechanism that pauses the system when there’s a big drawdown. Finally, only increase position sizes after verified positive performance across numerous trades.

The Role of AI and ML in Modern Trading Algorithm Software

Stock algorithm software has changed significantly. Rule-based systems still work, but the competitive edge increasingly belongs to systems that can adapt.

AI and ML applications in algorithmic trading include:

- Sentiment analysis — NLP models that parse news feeds, earnings call transcripts, and social data to generate trading signals before price movements occur.

- Reinforcement learning — agents trained to optimize strategy parameters dynamically based on changing market conditions, rather than fixed rules.

- Pattern recognition — deep learning models that identify chart patterns and anomalies across thousands of instruments simultaneously.

- Predictive modeling — regression and classification models that estimate price direction, volatility, or volume based on historical feature sets.

Integrating these capabilities requires more than just plugging in a model. You need clean, reliable data pipelines, proper model validation and feature engineering relevant to your strategy and proper model validation. This is where working with a team experienced in AI/ML-based custom trading platform development pays off.

CMARIX develops automated trading systems tailored to diverse trading needs.

Technical Requirements for Building an Algo Trading System

Here is what the build actually needs, beyond the strategy logic:

- Historical data – For backtesting trading algorithms, you need at least 5-10 years of tick or OHLCV data. The data source really matters too, since there’s survivorship bias, and free data can have gaps or adjustments that are just wrong.

- Real-time data feed – low-frequency systems can use REST APIs. If you need sub-second data, though, go for WebSocket connections; they’re standard. You’ve got options like Polygon.io, Refinitiv, and even direct feeds from exchanges.

- Execution infrastructure – Broker APIs let you route orders straight to exchanges. To get super-low latency, colocate your server in the exchange’s data center; this cuts execution lag significantly.

- Tech stack – Most algo traders choose Python for its extensive libraries like Pandas and NumPy, and quick prototyping. Also, the community help is great. Still, they use C++ when super speedy executions matter, you know, microseconds fast.

- Risk management layer – Safeguards like max drawdown limits, preventing duplicate orders, position size caps, and a halt on trading when losses hit preset levels are non-negotiable.

- Compliance layer – In the US, the SEC governs automated trading under frameworks like Regulation SCI, which sets infrastructure resilience standards for key market participants, alongside Rules 9 and 10 of the Securities Exchange Act of 1934.

Why Choose CMARIX for Custom Algorithm Trading Software Development?

Building trading algorithm software is one thing. Building it so it holds up under live market conditions with real latency, real data inconsistencies, and real money on the line is a different challenge entirely.

CMARIX has worked with fintech companies and trading firms to build automated systems that go well beyond a working prototype. From broker API integration and backtesting infrastructure to AI-driven signal generation, the team brings hands-on experience with the full stack a production trading system actually needs.

A few things that matter here: CMARIX works as an extension of your team. You get full transparency into architecture decisions, code ownership, and the ability to scale or change the systems as your strategy evolves.

If compliance is a concern, CMARIX builds regulatory checkpoints into the system from the start, not bolted on at the end.

Conclusion

Building custom algorithm trading software is a serious technical undertaking, but the payoff of consistent execution, zero emotional bias, and the ability to run strategies at scale, makes it worth doing properly. The mistake various teams make is rushing from strategy idea to live trading without investing enough in risk controls, backtesting, and infrastructure. Those shortcuts show up fast once real money is involved.

If you’re clear on your strategy and ready to build something production-grade, the architecture decisions and steps covered in this guide give you a solid starting point.

FAQ on Building Custom Algorithm Trading Software

What are the core benefits of building custom algorithm trading software?

Speed, consistency, and scale. A custom system executes at machine speed, follows the strategy exactly without emotional deviation, and can monitor more instruments than any human trader. It also gives you full control over the strategy logic — something no off-the-shelf platform can offer.

Which programming language is best for algorithmic trading?

Python for most use cases — it is fast to develop, has deep library support, and handles the data processing and ML workflows common in modern stock market algorithm software. C++ is the choice when execution latency is a primary constraint, such as in HFT systems.

How do I get reliable, real-time market data?

Through a dedicated market data provider via WebSocket (for streaming) or REST API (for snapshot data). Polygon.io, Interactive Brokers, and Refinitiv are commonly used. Avoid free sources for production — data quality issues will cost more than the subscription.

What is backtesting, and why is it critical?

Backtesting runs your algorithm against past price data to see how well it performs, without risking any actual money. This way, you spot bad logic, unrealistic assumptions, and tricky edge cases. If you skip this, you’re trading blindly. Always use out-of-sample data to prevent overfitting, though.

How do I connect my software to a broker to execute trades?

Via broker API — most major brokers (Interactive Brokers, Alpaca, TD Ameritrade) offer REST or FIX protocol APIs for order submission and account management. Algorithmic trading API integration is the bridge between your strategy engine and actual execution.

What risk management features must be hardcoded?

The maximum daily loss limit that stops trading when reached, plus a cap on per-trade position size. Duplicate orders must be prevented, and there should be an accessible kill switch without code deployment. Abnormal behavior alerts are essential, too.

Do I need a special server to run my trading bot?

For most strategies, a cloud VPS with low latency to your broker is sufficient. AWS or Google Cloud instances in regions close to major exchanges work well. For HFT, co-location in the exchange’s data center becomes necessary — latency differences of milliseconds can make or break strategy performance.