Quick Summary: Account-to-Account (A2A) payments enable direct bank transfers, cutting costs and delays compared to card payments. This guide covers A2A payment software development steps, tech stacks, benefits, use cases, and future trends for fintech success.

Money doesn’t move at the speed of the banks anymore; it moves at the speed of the customers’ expectations. Every touch and click now requires instant, invisible, and irrevocable transactions. Yet, many of the world’s payments still use the old card infrastructure, which is now a decade old.

This is a gap that, in turn, fuels the shift to Account to Account payments. Indeed, a report by Boston Consulting Group finds that real-time A2A already powers nearly a quarter of all global retail digital transactions, while adoption has exceeded 50% in markets such as India and Brazil, on the back of systems like UPI and Pix.

In this blog, we will cover:

- What A2A payments are and how they differ from traditional card-based systems

- Why legacy card networks are showing their age in a real-time world

- The key infrastructure and technologies driving A2A adoption

- A practical, step-by-step guide on Account to Account payment software development

- The major benefits A2A unlocks for businesses and consumers

- Core use cases where A2A delivers the most impact

- Forward-looking trends, including A2A with CBDCs, embedded finance, and AI-driven fraud prevention

- How CMARIX brings deep A2A development expertise to real-world solutions

Understanding Account-to-Account (A2A) Payments

In essence, an Account-to-Account transfer involves money being transferred from one bank account to another without passing through the Visa or Mastercard networks.

Unlike card payment systems, which have multiple participants who include the issuers, acquiring banks, payment schemes, and finally payment processors, A2A payment processing systems create a direct connection between the payer and the payee. When authorization occurs, it happens in real time, and confirmation is made immediately.

What Makes A2A Payments Different

A2A payments stand apart from traditional payment methods in several important ways:

- Transfer money between accounts directly

- Authorization by secure bank authentication

- Settlement occurs within immediate or near real-time

Settlement takes place in real time or near real time. It is done in real time or near real time. The process takes place in real-time or very close to it. For example, the need to specify card numbers or cards will not be necessary. The efficiency gained from implementing this type of organization is exactly what A2A Payments is now achieving, making it appropriate not only for business/financial systems but also for consumers.

Why the Traditional Card Model Is Showing Its Age

Structural Limitations of Card Payments

Despite their ubiquity, card payments come with inherent limitations:

- Delayed settlement: Funds can take days to actually reach merchants

- High interchange fees: Multiple parties take a cut of every transaction

- Chargebacks and fraud exposure: Merchants carry significant risk

- Complex infrastructure: Cards require tokenization, PCI compliance, and network routing

As digital commerce scales and customer expectations rise, these constraints are becoming increasingly visible.

The Cost Problem

For merchants, interchange and processing fees can range from 1.5% to 3.5% per transaction. At scale, this becomes a material drag on margins, especially in industries with thin profit models such as eCommerce, marketplaces, and digital services.

A2A payments reduce or eliminate many of these costs by bypassing card schemes entirely. To understand how to optimize the cost to build AI-based accounting software, you should connect with a professional A2A payment software development company.

A2A Vs Card Payments

| Comparison Area | A2A Payments | Card Payments |

| Transaction Flow | Direct bank-to-bank transfer via regulated payment rails | Involves issuing bank, acquiring bank, card network, and processor |

| Authorization Method | Secure bank authentication (OTP, biometrics, banking app approval) | Card details, CVV, 3D Secure, fraud screening layers |

| Settlement Speed | Real-time or near-instant settlement | Typically 1–3 business days for final settlement |

| Cost Structure | Low rail fees, no interchange, fewer intermediaries | 1.5%–3.5% including interchange, network, and processor fees |

| Fraud & Chargebacks | Lower fraud exposure, usually irrevocable once confirmed | Higher fraud risk, chargebacks can reverse funds weeks later |

| Infrastructure Requirements | API integrations, webhook handling, reconciliation systems | PCI compliance, tokenization, network routing, fraud tools |

| Best Suited For | B2B payments, marketplace payouts, subscriptions, real-time transfers | Retail purchases, global acceptance, consumer familiarity |

The Core Pillars that Power A2A Payments

A2A payments are not a single technology but an ecosystem built on modern banking rails, real-time payment networks, and open banking frameworks.

Real-Time Payment Rails

Many countries now operate real-time payment infrastructures that make A2A possible at scale:

| System | Region | Launch Year | Settlement Speed | Cross-Border Support |

| UPI | India | 2016 | Instant (seconds) | Limited (expanding internationally) |

| Faster Payments | UK | 2008 | Near-instant (seconds) | No (domestic UK only) |

| SEPA Instant | Europe (Eurozone) | 2017 | ≤10 seconds | Yes (within participating Eurozone countries) |

| Pix | Brazil | 2020 | Instant (seconds) | No (domestic Brazil only) |

| RTP | United States | 2017 | Instant (seconds) | No (domestic US only) |

| FedNow | United States | 2023 | Instant (seconds) | No (domestic US only) |

Open Banking and APIs

The next step in creating a peer-to-peer payment application is selecting the most appropriate transaction method. A2A payment routes the money directly between different bank accounts. This opens up the ability to carry out open banking in more and more countries.

A2A payments can be a great boon for fintech companies in particular. It allows them to withdraw funds directly from the consumer’s account rather than relying on cards. Typically, A2A payments are made via a secure API connection between the banks and the fintech payment solutions.

With open banking APIs, platforms are able to:

- Make payments directly from your bank account, without needing cards.

- Verify user safety using modern security methods such as OAuth and Strong Customer Authentication (SCA).

- Get an instant confirmation once the payment is made.

- Check your balance in real time to stay up to date.

- Easily access detailed transaction data for quick and accurate reconciliation.

Connect with CMARIX to build your next custom banking software solution.

Build Banking SoftwareSecure Authentication and Consent

A2A payments rely on strong customer authentication rather than static card credentials. Payments are authorized using bank-grade security measures, including biometric verification, multi-factor authentication, and app-based approvals.

This shifts security from “what someone knows” (a card number) to “who someone is” (verified account holder), reducing fraud vectors tied to stolen card data.

Consent is explicit, traceable, and time-bound. Users approve exactly when and where money moves, and once completed, transactions are final.

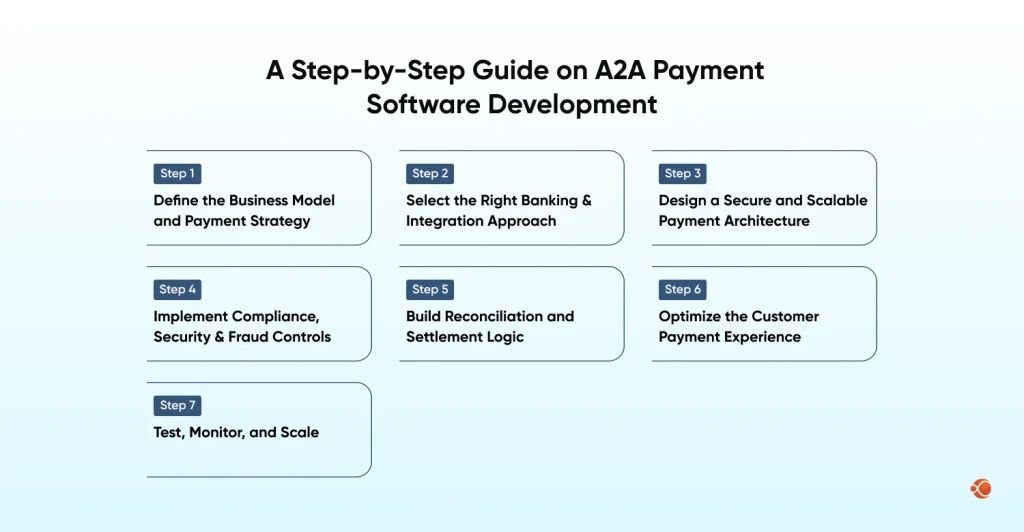

A Step-by-Step Guide on Account-to-Account Payment Software Development

Step 1: Define the Business Model and Payment Strategy

Before building A2A payments, understand your purpose: collections, payouts, or subscriptions. Consider where you operate, if real-time payments are required, expected transaction volume, and average amount. If these factors are not clear from the start, the system may need to be redesigned later.

Step 2: Select the Right Banking & Integration Approach

| Integration Method | Description |

| Direct Bank Integration |

|

| Open Banking APIs |

|

| PSP/Aggregator Integration |

|

Step 3: Design a Secure and Scalable Payment Architecture

Developing appropriate infrastructure is necessary for establishing a sustainable digital A2A payment system. Digital A2A payment infrastructures face serious breakdowns that reflect the following current issues: “payment confirmations are long; intersystem communication is not effective; security levels of digital A2A payments are higher than the security needs of other payments.” Once the entire system is reduced to a failure state, minor failures may trigger larger system failures involving “duplicated payments, payment notifications without confirmation, and serious accounting failures.”

Key components of an effective A2A architecture include:

| Component | Description |

| Payment Orchestration Layer | Manages the flow of payments across different systems. |

| Secure Bank/PSP Connectors | Ensures safe and reliable connections to banks or payment service providers. |

| Webhook Listener & Validation System | Receives payment updates and verifies transaction status. |

| Internal Transaction Ledger | Records all payment activities internally for tracking and transparency. |

| Reconciliation Engine | Matches internal records with bank data to ensure accuracy. |

| Fraud Monitoring System | Detects suspicious activity and helps prevent fraudulent transactions. |

Step 4: Implement Compliance, Security & Fraud Controls

A2A payments are subject to strict financial regulations.

Implementation must account for:

- KYC/KYB workflows

- AML monitoring

- SCA (Strong Customer Authentication)

- RBI / PSD2 / NACHA / regional regulatory rules

- GDPR and data protection

Security layers should include:

- OAuth 2.0 / mutual TLS

- Webhook signature validation

- Rate limiting

- Velocity checks

- Anomaly detection

A professional financial software development company ensures compliance is embedded in the system, not added later as a patch.

Step 5: Build Reconciliation and Settlement Logic

This is the most underestimated part of A2A implementation.

Unlike card payments:

- Confirmation can be asynchronous

- Settlement windows vary

- Reversals are limited

- Refunds follow different rails

The system must support:

- Real-time webhook confirmation processing

- Automated ledger updates

- Bank statement matching

- Settlement report generation

- Mismatch detection alerts

Manual reconciliation does not scale. Automated reconciliation separates stable payment systems from unstable ones.

Step 6: Optimize the Customer Payment Experience

A2A adoption depends heavily on user experience.

The payment flow should:

- Minimize redirects

- Support mobile deep linking

- Clearly display payment status

- Auto-detect success via webhook

UX improvements directly affect conversion rates, drop-off rates, and payment success rates. A well-designed experience can significantly increase A2A adoption compared to card-based flows.

Step 7: Test, Monitor, and Scale

The A2A API-based payment solutions require extensive test cases to confirm that all possible edge cases in the real world are covered. However, to make the payment system more secure against fraud, you will need to hire dedicated developers who cover all test cases and ensure its security.

Key Benefits of A2A Payments

| Benefit | Description |

| Drastically Reduced Costs | Skip card networks and middlemen to slash interchange fees and transaction expenses. |

| Lightning-Fast, Real-Time Transfers | Funds zip between accounts in seconds, eliminating multi-day waits from legacy systems. |

| Superior Security, Minimal Fraud | Bank-direct authentication with biometrics and MFA sidesteps card data theft and phishing. No need to store sensitive details. |

| No More Chargeback Headaches | Transactions lock in as final, meaning merchants avoid disputes, refunds, and paperwork. |

| Boosted Cash Flow | Instant settlements unlock funds immediately, enhancing liquidity and operations. |

| Frictionless Customer Experience | Seamlessly embed payments in banking apps for one-tap convenience. |

| Higher Transaction Ceilings | Handle big-ticket payments effortlessly, free from card network limits. |

Core Types of A2A Payments: Where A2A Payments Deliver the Most Impact

| Type | Explanation | Real-World Examples |

| Business-to-Business (B2B) |

|

|

| Business-to-Consumer (B2C) |

|

|

| Peer-to-Peer (P2P) |

|

|

| Consumer-to-Business (C2B) |

|

|

How CMARIX Brings A2A Digital Payment Systems Development Expertise

CMARIX is an award-winning custom software development company that makes Account-to-Account (A2A) payments simple and seamless, especially for fintech, e-commerce, and growing businesses.

They excel at building integrations with global payment rails like UPI, SEPA Instant, Pix, RTP, and FedNow. This lets you transfer funds in over 50 currencies in real time, without needing local bank accounts in every country. Our payment API integration development services cover everything from payment initiation APIs and secure open banking authentication to handy reconciliation dashboards.

Thanks to their expertise in robust backend systems, CMARIX helps slash middleman fees, settle payments in seconds, and stay fully compliant with local rules. Businesses love the faster cash flow and easy scaling for B2B, B2C, or P2P needs.

These solutions blend seamlessly with your existing cards and wallets through clean, unified dashboards, powered by modern tech such as React, Node.js, and cloud infrastructure.

The Future of A2A Payments: What Comes Next

| A2A Synergy | Synergy Explanation |

| A2A + CBDCs | A2A pairs with digital government money (CBDCs) for fast, smart transfers. Wallets link to banks easily. Governments send aid or refunds instantly. Speeds up global payments. A2A connects old banks to new digital cash. |

| A2A + Embedded Finance | A2A adds banking inside apps like shopping sites or gig work. Gives quick payouts to sellers, workers pay in one click, easy subscriptions. Apps handle money without cards. |

| A2A + AI Fraud Protection | A2A stops card scams but needs quick checks. AI watches for weird spending, fast bursts, bad accounts. Scores risks fast and learns from users. Keeps speed high, no slowdowns. |

Final Words

A2A payments mark the dawn of a faster, fairer financial system, stripping away outdated layers to deliver instant, secure, and cost-effective money movement. Businesses that embrace this shift today will lead tomorrow’s digital economy, while those clinging to card networks risk falling behind.

Take Action Now for Future of Digital Payments:

- Audit your current payment fees and settlement times.

- Pilot A2A in one high-volume use case, like payouts or B2B invoices.

- Partner with experts like CMARIX for compliant, scalable implementation.

FAQs on Account-to-Account Payment Software Development

What are account-to-account (A2A) payments?

Account-to-Account (A2A) payments move funds directly between bank accounts, skipping cards or processors. They enable fast, low-cost transfers via open banking rails like UPI or SEPA.

What is account-to-account payment software development?

Building software to integrate direct bank transfers using APIs from open banking, PSPs, or rails. Covers orchestration, compliance, and reconciliation for real-time A2A flows.

Which technologies are used in A2A payment software development?

Node.js/React for frontends, Python for reconciliation, cloud (AWS) for scaling. Open banking APIs, OAuth security, webhooks for status updates.

Which industries benefit most from A2A payments?

Fintech, e-commerce, and gig economy lead adoption for payouts, invoices, and subscriptions. B2B suppliers and insurers gain from instant settlements.

Can A2A payments be used for international transactions?

Yes, via global rails like SEPA, Pix, RTP across 50+ currencies without local accounts. Real-time cross-border via UPI or FedNow links.

How long does it take to develop an A2A payment solution?

Timelines vary by scope; contact CMARIX for a custom quote tailored to your needs, compliance requirements, and integration complexity. They deliver fast, scalable solutions.

Can A2A payment software be integrated with existing systems?

Yes, via unified APIs blending A2A with cards/wallets on dashboards. Webhooks handle async confirmations; microservices ensure scalability.