Quick Summary: The insurance claims processing automation in 2026 is transforming the carrier performance with the help of AI-based FNOL, intelligent routing, document AI, reserve modeling, fraud analysis, and real-time dashboards, which can potentially reduce the cycle time by up to 75%, cost by 30-40%, and increase the policy retention.

Two-thirds of U.S. insurers are watching a transformation unfold rather than leading it. McKinsey’s 2025 analysis of AI in insurance puts full AI adoption at just 34% across the industry (up from 8% the year prior), while digital leaders like Aviva have already saved over £60 million by deploying more than 80 AI models across their claims domain.

The gap between leaders and others is widening fast. The J.D. Power 2025 U.S. Property Claims Satisfaction Study found that average claim cycle time has reached 44 days, the longest on record. Per the J.D. Power 2025 Claims Digital Experience Study, 52% of policyholders who rate their digital claims experience as poor are likely to leave. Only 4% of those with an excellent experience say the same.

In This Blog, You Will Get Answers To:

- What are the reasons that legacy claims systems will not be effective in 2026?

- How would you describe a fully integrated automated claim management system based on advances in Artificial Intelligence?

- What can an Insurer do to reduce claim processing time and costs per claim by 30-75%?

- What is the relationship between automating the First Notice of Loss and Straight Through Processing and Return on Investment for Insurers?

- In what ways can Artificial Intelligence improve the accuracy of reserves and the detection of fraud throughout the organization?

- What is needed for insurers to have real-time visibility into their claims processes?

- What type of phased implementation will provide the insurer with the fastest and most cost-effective path to achieve the implementation of their claims solution?

2025 Benchmark Snapshot

- AI-enabled carriers have cut claim resolution time by 75% (from 30 days to 7.5 days) and reduced cost per claim by 30-40%, from $40-60 to $25-36. Source: Datagrid / BCG Research, December 2025.

Why Legacy Claims Systems Are Failing in 2026

The claim infrastructure legacy infrastructure remain function but does not fail all at once; it fails gradually, in several ways at the same time (costs are going to go up, reserve estimations are going to become less accurate, and there is no longer an expectation of having real-time visibility of the claims process by policyholders).

Three structural problems define the crisis in 2026:

Data Fragmentation Is Destroying Operational Productivity

At present, most carriers operate 4 to 7 separate systems across disparate applications to run their organisations, e.g., policy administration, claims management, billing, underwriting, fraud detection, and multiple third-party vendor applications. According to research conducted by McKinsey’s insurance modernization team, upgrading these infrastructures will deliver a 41% reduction in per-policy IT costs and also 40% increase in operational productivity. In 2025, approximately 74% of the insurers will still be operating on their legacy core systems.

According to a recent study, in a non-automated claims process, manual document handling accounts for up to 80% of total time spent processing claims. The downstream effects are significant

- The accuracy of reserves deteriorates, as policy and claims data are not synchronised in real-time

- Frequently missed subrogation opportunities occur due to siloed workflows created by adjusters

- Compliance SLAs require manual tracking, leading to regulatory risk at scale

Policyholder Expectations Have Permanently Reset

According to the J.D. Power 2025 U.S. Insurance Digital Experience survey, the percentage of auto insurance claims management software bought from websites has increased from 35% to 47% and exceeded purchases made through other traditional channels, such as agents (35%) and call centers (17%); thus, a significant portion of people will not review any claims made through an analog channel.

Proactive communication data is alarming: only 22% of all insurers provide sufficient digital claim status updates, despite proactive claim status updates being the number one factor contributing to customer satisfaction in 2025. The discrepancy is resulting in a tangible, measurable difference in renewal rates.

Fraud Is Outpacing Manual Detection Methods

Insurance fraud in the US is estimated to cost $308.6 billion a year, according to the Coalition Against Insurance Fraud (CAIF). The National Insurance Crime Bureau (NICB) predicts that identity-related fraud will increase by 49% by 2025 due to synthetic identities and artificial intelligence (AI) generated documents being undetectable by traditional rule-based detection methods.

| Problem Area | 2025 Figure | Source |

| Average claim cycle time | 44 days | Record high, J.D. Power 2025 |

| Carriers still on legacy technology | 74% | McKinsey 2025 |

| Policyholders at churn risk (poor digital experience) | 52% | J.D. Power 2025 |

| Annual U.S. fraud losses | $308.6 billion | CAIF 2025 |

| Projected rise in identity-linked fraud | 0.49 | NICB 2025 |

| Proactive digital update delivery rate | 22% | J.D. Power 2025 |

| Full AI adoption rate in insurance | 34% (up from 8%) | McKinsey 2025 |

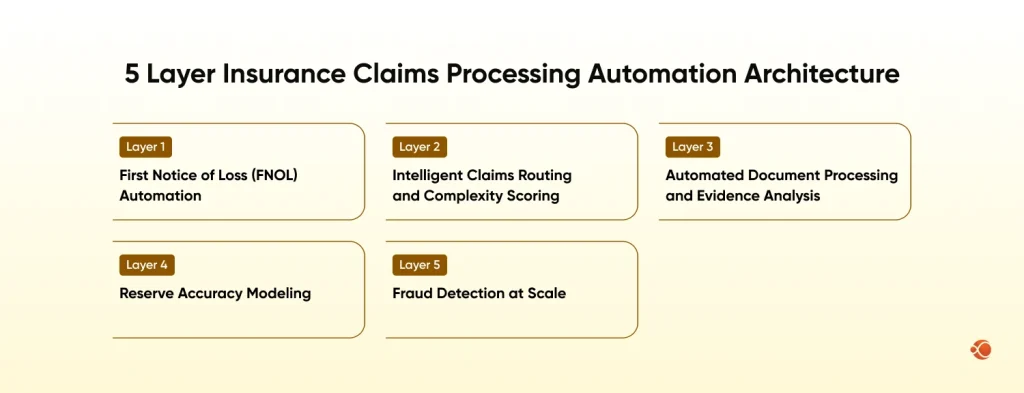

The 5 Layer Insurance Claims Processing Automation Architecture

Insurance claims processing automation is not a single product purchase. It is a layered architecture where each capability multiplies the value of the next. The sequencing matters as much as the technology.

When evaluating different service models for custom software development, companies often fail to consider the importance of the order in which they deploy each of the five layers shown below. It has been shown that the sequence defined in the following layers provides the fastest ROI across enterprise implementations.

Layer 1: First Notice of Loss (FNOL) Automation

FNOL represents the highest-volume and most automated entry point within the claim lifecycle. With AI-driven intake engines that collect claims from all input sources (phone transcriptions, web forms, insurance mobile app implementations, email, third-party API feeds), creating structured data takes seconds rather than hours.

FNOL is the most voluminous and automatable point in the claims process. AI-powered intake engines process claims from all channels (phone transcription, web forms, insurance mobile app development output, email, and third-party API feeds) and extract structured data in seconds, not hours.

What changes operationally with automated FNOL:

- Reduction of up to 80% in manual intake processing for standard claims

- Claims triage is achieved within minutes of submission, irrespective of the channel

- Consistency in data extraction quality, irrespective of the number of staff or the change of shifts

- Straight feed into routing, reserving, and fraud scoring without re-keying

For a detailed analysis of intake architecture and vendor choices, our guide to AI in insurance intake automation is the best resource.

Layer 2: Intelligent Claims Routing and Complexity Scoring

The AI routing engines rate incoming claims on five criteria and route them to the appropriate processing path, without human triage for most claims. This is where claims automation for auto insurance app development and personal lines volume really starts to pay off.

| Scoring Dimension | What It Measures |

| Severity | Estimated loss magnitude based on loss type and coverage limits |

| Complexity | Number of parties, jurisdictions, and coverage overlaps involved |

| Fraud Risk | Graph-based anomaly score versus known fraud patterns and networks |

| Litigation Probability | Based on injury type, attorney involvement signals, and jurisdiction history |

| STP Eligibility | Composite score determining automated settlement candidacy |

Claims management automation solutions powered by AI can now process 70-90% of simple personal lines claims straight through, with decisions rendered in minutes. The reduction in adjuster staff resources due to this routing efficiency is usually redeployed to complex, high-value claims, where human judgment leads to improved outcomes.

Layer 3: Automated Document Processing and Evidence Analysis

Modern insurance claim management software with document AI processes police reports, medical records, repair estimates, photos, and video evidence at 95%+ accuracy for standard document types. Our insurance document AI comparison guide covers the leading platforms in detail.

The operational shifts when document AI is deployed at scale:

- The manual processing of documents has reduced from 80% to a minimum of 20% of the total processing time

- Policy term cross-referencing happens at intake rather than during adjudication

- Missing documentation and coverage gaps are flagged before adjuster assignment

- Full audit trails are automatically generated for each document review decision

Layer 4: Reserve Accuracy Modeling

Inaccuracy in reserve estimation is a quiet source of lost profitability. When you over-reserve, you essentially lock away funds. On the other hand, under-reserving can result in unfavourable outcomes that affect combined ratios and attract regulatory attention.

Machine learning in fintech, as applied to insurance reserve estimation, mitigates both failure modes concurrently. AI models refine their estimates of the settlement range based on incoming documentation, medical, and repair data.

McKinsey projects a 25-30% reduction in loss adjustment expenses and a 3-5 percentage point decrease in indemnity spend for carriers deploying AI-driven reserve modeling, figures that represent enormous capital release for carriers running multi-billion-dollar portfolios.

💡 Capital Release Math

- An improvement of 5% in the accuracy of reserves for a $500M portfolio of claims will free up $25M in capital. Most AI reserve solutions will pay for themselves on this basis alone within 12-18 months of going live.

Layer 5: Fraud Detection at Scale

Rule-based fraud detection systems are ineffective against the synthetic identity and AI-created document vectors that are fueling the expansion of organized fraud in 2025. Graph neural networks, which are the backbone of contemporary claims management automation systems, can identify connections among claimants, providers, attorneys, body shops, and medical facilities to reveal ring structures that would never be identified through individual claim analysis.

Building Real-Time Claims Visibility: The Integration Architecture

AI capabilities deliver value proportional to the data they can access and act on in real time. The integration layer is not a supporting concern. It is the foundational constraint that determines what is possible at every automation layer above it.

API-First Architecture: The End of Batch Processing

Carriers interested in software for automating claims processing are replacing batch ETL with event-driven, API-first processing. Every status change, payment approval, document receipt, and fraud indicator is automatically distributed in real-time across policy admin, claims, billing, and analytics systems.

According to Forrester’s 2025 insurance technology forecast, spending on insurance technology is set to grow by 8% in 2025, with the highest growth in integration middleware and cloud-native platforms. EDI Integration for insurance claims automation is an essential part of this layer, enabling the real-time standardization of structured data exchange with healthcare providers, repair networks, and law firms.

What a Data-Driven Dashboard for Insurance Companies Looks Like in Practice

When the integration layer is properly constructed, all stakeholders receive what they need, when they need it, without having to wait for batch reports or status calls. Below is a list of what a data driven dashboard for insurance companies can provide for various stakeholders:

Claims Adjusters

- Live view of assigned claims and total workload

- Automatic notifications of new documents received

- AI-driven reserve guidance to inform decisions

- Real-time fraud notifications to focus on high-risk claims

- Crystal-clear visibility to expedite claims resolution and minimize delays

Operations Managers

- Real-time SLA performance tracking

- Aging claim reports and cycle time trends

- Team capacity and workload heatmaps

- Early visibility into bottlenecks before they escalate

- Data-driven insights to balance resources effectively

Finance / Actuarial

- Reserve exposure visibility by line of business

- Early alerts on adverse development trends

- Portfolio-level risk dashboards

- More accurate forecasting and capital allocation insights

Compliance

- Real-time monitoring of regulatory deadlines

- Full audit trail of every decision made

- Automatic notification of exceptions

- Minimized regulatory risk and effort to monitor compliance

Policyholders

- Real-time status updates for claims

- Simple access to document upload functionality

- Alerts regarding the various steps of your claim

- Instant payment confirmations

- No hassle process for submitting your claim online

CMARIX delivers AI-driven claims automation, real-time visibility, and measurable ROI across the entire claims lifecycle.

Contact UsThe Policyholder Portal: Retention ROI in Plain Numbers

The J.D. Power 2025 Claims Digital Experience Study is unambiguous: 52% of customers with a poor digital claims experience are at risk of churn, versus just 4% with an excellent one.

Currently, only 36% of auto insurance customers and 31% of homeowners’ customers receive claim status updates via their insurer’s mobile app. Closing this gap with proactive, automated milestone communications not only improves satisfaction scores but also improves overall performance. It compounds retention advantages that become increasingly difficult for slower-moving competitors to close.

What AI Claims Automation Is Actually Delivering: 2025 Benchmarks

| Metric | Legacy Baseline | With AI Automation | Improvement |

| Claim resolution time | 30 days | 7.5 days | 75% faster |

| Routine claim processing | 7-10 days | 24-48 hours | 70-80% faster |

| Standard cost per claim | $40-60 | $25-36 | 30-40% lower |

| Complex cost per claim | $200+ | $120-140 | 30-40% lower |

| Manual document handling | 80% of time | 20% of time | 75% reduction |

| STP rate (simple claims) | 10-15% | 70-90% | 5-6x improvement |

The Aviva rollout (as indicated in the McKinsey 2025 Report) is the most widely documented case study of a large carrier. The following outcomes resulted from the process of scaling to more than 80 AI models for motor claims:

Time to determine liability: 23 days reduced on complex cases

- Accuracy of claims routing: 30% improvement

- Customer complaints: 65% reduction

- Total documented value: over £60 million ($82 million) in a single year

The trend continues by carrier size and geography: the ROI business case for enterprise digital transformation consulting in claims is among the strongest in financial services.

How CMARIX Has Delivered Insurance Transformation: Real-World Case Studies

The performance benchmarks above reflect industry-wide AI adoption trends. What follows is how CMARIX has translated those outcomes into working production systems for insurance carriers and digital insurance platforms across three continents. Here are some examples of our AI-driven claims automation solutions:

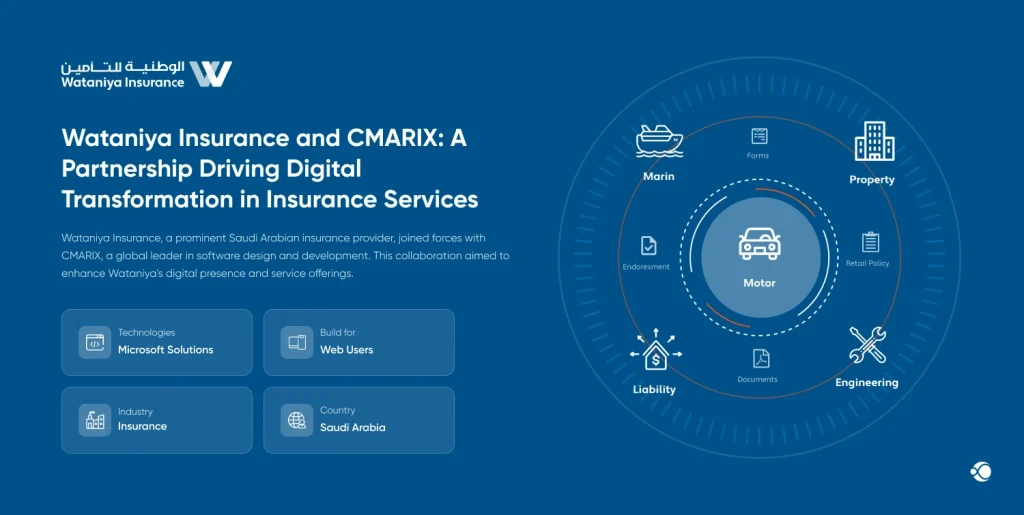

Wataniya Insurance: Saudi Arabia

Paper-Based Operations → Enterprise Claims Platform

Challenge: Wataniya used paper-based processes to manage all operations. With increasing operational volume, there were errors in retrieving information, policyholders lacked an online facility to access, and difficulties complying with regulations.

CMARIX Solution: CMARIX designed and developed a completely customized insurance management system with multi-role login functionality, automated commission processing, and a secure policyholder login facility for online claim submissions and status tracking.

Result: The operations were transformed from completely paper-based to completely digital, with no manual handling of documents, the ability to track policies and claims in real time, and a compliant, scalable platform now used as the primary interface for both individual and corporate policyholders.

Beema1: Digital Insurance Platform

Manual Claims Workflows → Automated, Fraud-Aware Claims Engine

Challenge: Beema1 needed a new, modern way to process claims through a fully automated claims processing and service delivery platform with integrated fraud detection capabilities, real-time claim status updates, and no abuse related to legacy systems.

CMARIX Solution: CMARIX provided automated claims processing with integrated fraud detection at intake, a dynamic policy configuration engine, and customer-facing portals with real-time claim status updates.

Result: The processing time for claims was significantly reduced, the point of fraud detection moved from post-adjudication to intake, and the self-service portal improved policyholder satisfaction scores.

Aspen Claims: Claims Management Platform

Legacy Systems → End-to-End Claims Lifecycle Platform

Challenge: The challenge for the client was to have a specific platform to manage the entire claims process, from FNOL to final settlement, with real-time workflow visibility, which was not possible with legacy systems.

CMARIX Solution: CMARIX developed a web-based claims management platform with automated intake triage, document management with complete audit trails, and real-time dashboards for adjusters and operations managers.

Result: The overhead on the adjuster workflow was reduced substantially, operations management had real-time visibility into claims, and the document management trail was audit-ready, which paved the way for STP in the next phase.

AI Claims Management Questions You Should Know Answers for in 2026

What is the most popular insurance claims management software most suitable for large carriers?

Choosing the best insurance claims management software platform is based on factors such as your line of business, current core system architecture, API maturity, and whether your carrier needs an individual solution or a complete suite. There is no singular answer to what is best. However, the structured evaluation framework allows for evaluating different platforms to find the best-suited option for each situation.

Key criteria for enterprise-grade insurance software development services:

- Integration with popular policy administration systems (Guidewire, Duck Creek, & Majesco).

- Providing an understanding of policies and some form of documentation for regulations.

- Pre-trained models, compared to models that need only carrier-specific data.

- Real-time API connection vs. the limitations of batch processing.

- STP rate benchmark for all lines of business from live deployments that can reference other companies.

Our 2026 Insurance Claims AI Vendor Evaluation Framework covers 47 capability criteria across the leading platforms.

What is straight-through processing (STP), and what rate should we target?

Straight-through processing (STP) means a claim that has no manual assistance (i.e., was able to be processed without any human intervention) and has gone through the entire process, from the claim being assessed to the reserve being set, to the claim being approved/denied, to the actual payment of the claim.

The STP rate serves as a primary productivity benchmark for insurers that are using machine-learning-enabled claims software.

By 2025, the leading auto insurance companies will have identified an STP rate of 70% to 90% for basic personal auto claims (i.e., auto claims with the least complexity).

According to IDC’s projections, the STP rate for all auto, homeowners, and commercial auto claims will be at least 65% by 2026.

How does EDI integration for insurance claims automation work?

Electronic Data Interchange (EDI) is a means for facilitating the exchange of structured (i.e., machine-readable) data between insurance organizations, health care organizations, automotive repair networks, attorneys’ offices, and governmental authorities in a uniform manner.

The use of EDI will enable real-time exchange of structured (i.e., machine-readable) data between the process and fraud detection components of an automated claims architecture.

Critical EDI integration considerations:

- ANSI X12 and EDIFACT compliance for healthcare and property claims

- To achieve STP at scale, companies must have the ability to process EDI transactions in real time; therefore, real-time EDI must be available

- The vendor portal will facilitate EDI transactions between repair shops, medical providers, and attorneys

What ROI timeline should we expect from AI claims automation?

Most documented enterprise deployments achieve positive ROI within 12-24 months. Primary value drivers:

| Value Driver | Impact of AI Claims Automation |

| Cost per Claim | 30–40% reduction on standard lines through automation and reduced manual handling |

| Adjuster Capacity | 30–50% productivity improvement, allowing teams to handle higher volumes without increasing headcount |

| Fraud Prevention | Contributes to an estimated $44B in annual industry-wide savings through AI-powered detection |

| Litigation Expense | Lower legal costs driven by faster settlement of valid claims and improved decision accuracy |

| Retention Improvement | Converts up to 52% churn-risk customers (poor digital experience cohort) into satisfied, renewing policyholders |

The budgeting for digital insurance platforms must factor in both the direct cost savings and the compounding retention value of closing the digital experience gap. Those firms spending $25-100 million annually on AI capabilities (the range BCG sees for enterprise-scale investment) are outperforming their competition on combined ratio and customer retention.

Is AI claims automation compliant with state insurance regulations?

The NAIC has released an “AI Principles” framework that deals with transparency, explainability, and non-discrimination requirements. The state-level regulations regarding claims-specific AI are still evolving as of 2025-2026.

The insurers are mandated to ensure that their insurance claims automation systems provide complete decision audit trails and explanations for adverse decisions, in accordance with current fair claims practices statutes, which governance-first AI solutions developed in 2025 are expected to enable.

Your 2026 Phased AI-Insurance Claims Software Implementation Roadmap

The fastest carriers to achieve ROI through claims automation share one common feature: they aren’t tempted to try to do everything at once. A phased implementation will always exceed a large-bang implementation, both in terms of speed and cost.

| Phase | Capability Deployed | Expected Outcomes |

| Phase 1 (Months 1-4) | FNOL Automation | 60-80% FNOL automation; STP baseline established; integration layer built |

| Phase 2 (Months 5-10) | Document AI + Reserve Modeling | Manual handling drops 60%; reserve accuracy improves 20-30%; adjuster capacity freed |

| Phase 3 (Months 11-18) | Fraud Analytics + Policyholder Portal | Fraud detection rate up 30%+; customer satisfaction gains; full-scale STP reached |

1. Conduct a Claims Process Maturity Assessment

Map your current state before any vendor evaluation or investment. The metrics that matter:

- The current straight-through processing (STP) rate should be measured across each line of business to determine where automation is already effective and where manual intervention remains dominant.

- To determine baseline performance for speed, efficiency, and customer experience, calculate the average cycle time from FNOL through to Final Payment.

- The cost per claim, segmented between standard and complex cases, should be analyzed to identify operational inefficiencies and quantify potential automation savings.

- Fraud leakage should be measured as a percentage of written premium to determine the extent of preventable losses the company is currently incurring.

- The difference between initial reserve estimates and ultimate settled amounts should be evaluated to measure reserve accuracy and capital allocation effectiveness.

- Adjuster satisfaction levels and attrition rates should be reviewed to determine how workload, manual processes, and system limitations may be impacting workforce stability and productivity.

This baseline establishes your ROI goals and determines the deployment order. The telecom operators who were most successful with AI in 2025 began with governance-first programs to ensure that explainability and auditability were integrated into the design.

2. Prioritize FNOL Automation First

FNOL delivers the fastest time-to-value of any claims automation investment. It operates at the front of every single claim, has the highest density of repetitive, automatable tasks, and generates structured data that improves every downstream AI layer.

The 2025 Roots State of AI Adoption in Insurance survey found that FNOL is where carriers have made the most progress in their 2025 pilot initiatives. Most have achieved 60-80% automation within 6 months of deployment with the right tools.

3. Build the Integration Foundation Before Adding More AI

Event-driven API architecture is the precursor to all capabilities above Layer 1. Those carriers that bypass this step and continue to support legacy batch processing will be limited at every layer that follows, as fraud models will be unable to respond to real-time signals, reserve engines will be unable to update when documents are received, and the policyholder portal will be unable to display status.

Invest in the integration layer as infrastructure. The ROI compounds across every AI capability added afterward. It is the highest-leverage investment in the entire modernization program.

4. Pilot Fraud Analytics on One Line of Business

Fraud graph analytics require training data already available in your existing claims history. According to the National Insurance Crime Bureau, the use of identity theft in insurance fraud is expected to increase by 49% by the end of 2025, underscoring the need for insurers to take decisive action. Start by piloting your solutions on the line of business with the highest fraud exposure. Validate detection improvement against your baseline. Expand once the model is validated against live claims data.

Ready to Modernize Your Claims Operation with CMARIX?

The 2025 data have resolved the debate about whether it works. It does. Carriers with mature implementations are resolving claims 75% faster, spending 30-40% less per claim, catching more fraud materially, and retaining policyholders at structurally higher rates.

At CMARIX, we specialize in insurance software development services and large-scale enterprise application development for carriers at every stage of the modernization journey, from initial maturity assessment through full production deployment. Our team combines insurance operations expertise with fintech and software development opportunities to deliver programs that generate measurable outcomes, not just working code.

The enterprise digital transformation consulting practice at CMARIX provides consulting services to carriers across personal lines, commercial, specialty, and life and health business segments. Whether it is a full-stack claims transformation or an FNOL automation, we build for outcomes, not deliverables.

In 30 minutes, we will review your current claims metrics, identify your highest-value automation opportunity, and outline a realistic 90-day quick-win roadmap. No commitment required.

Book a CallConclusion

Insurance claims modernization is no longer a choice. In 2026, insurers using AI-powered claims automation are seeing claims resolved 75% faster, with 30-40% lower costs, and significantly improved retention through real-time visibility and communication.

Legacy architectures simply can’t compete with a layered, API-first, automation-centric architecture. The key to success is a phased rollout approach: FNOL first, followed by document AI, reserve modeling, fraud analytics, and a real-time policyholder portal.

The performance divide is growing. Speed of execution is now the determinant of competitiveness.

FAQs: Insurance Claims Automation Software

What is insurance claims automation?

Insurance claims automation uses AI, machine learning, and workflow software to automate tasks such as intake, review, fraud detection, and payment processing with minimal human intervention, reducing cycle time, costs, and errors throughout the entire claims process.

How does AI improve insurance claims processing?

It enables triage, routes claims in a smart way, extracts data from documents, assesses fraud risk in real-time, and models reserve accuracy dynamically. This enables faster settlements, reduced errors, lower cost per claim, and increased capacity for adjusters to handle high-value claims.

How long does it take to develop insurance claims management software?

A dedicated FNOL automation module would require 3-6 months for implementation. The overall end-to-end claims management software solution, including document AI, fraud analytics, and the policyholder portal, would require 12-18 months for implementation.

How much does it cost to develop insurance claims processing software?

Costs vary by scope, integrations, and line of business. Modular deployments typically start at $250,000-$750,000. Enterprise-scale platforms with custom AI models, legacy system integration, and multi-line support range from $1 million to $5 million or more.

Can you develop custom insurance claims automation software?

Yes. CMARIX build custom insurance software tailored to your lines of business, existing core systems, and regulatory environment. Every engagement starts with a maturity assessment to identify the highest-value automation opportunities before a single line of code is written.

Why should insurance companies invest in claims automation software?

Because the financial argument is clear. AI-powered carriers lower the cost per claim by 30-40%, close claims 75% faster, uncover much more fraud, and retain customers at a higher rate. Those carriers that delay are giving up market share to the competition.

Can insurance claims software scale as my business grows?

Modern cloud-native claims platforms are built for elastic scaling. Volume spikes from catastrophe events, new product launches, or geographic expansion are handled automatically. The AI models also improve as claim volume grows, making the system more accurate and efficient over time.